Financial Analytics · Time Series Forecasting

Benchmarking statistical and deep learning models (ARIMA, SARIMA, LSTM) for medium-term stock price forecasting using historical market data.

Financial institutions and investors rely on accurate forecasts of asset prices to support portfolio management, trading strategies, and risk assessment. However, financial time series are inherently volatile, non-stationary, and influenced by evolving market regimes. Traditional statistical models provide interpretability but may struggle with complex patterns, while deep learning approaches offer flexibility but require large datasets and careful tuning. Organizations therefore face a critical challenge: determining which forecasting methodology provides the most reliable predictions under real market conditions. A systematic comparison of statistical and machine learning models is needed to identify the most robust approach for medium-term stock price forecasting.

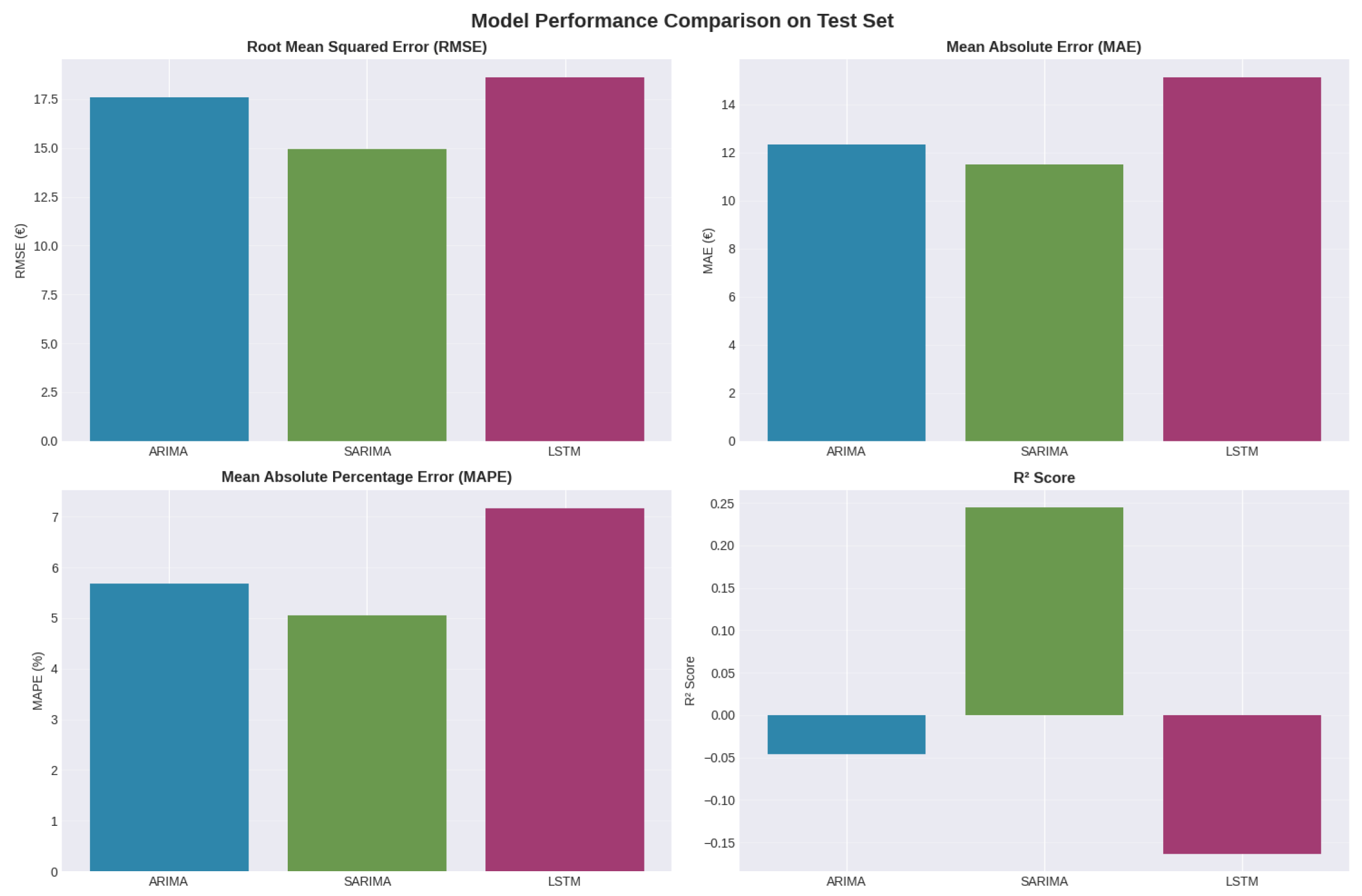

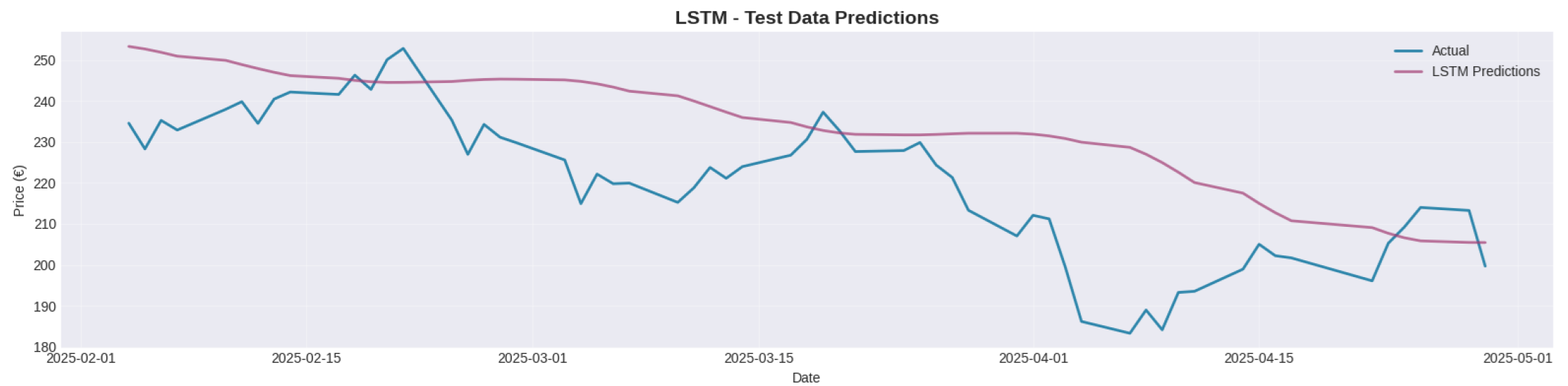

We conducted a comparative study of statistical and deep learning approaches for forecasting stock prices. Historical daily market data for Schneider Electric was collected and analyzed to understand temporal patterns, volatility, and seasonality. After preprocessing and exploratory analysis, the time series was transformed to achieve stationarity and then partitioned into chronological training, validation, and testing sets. Three forecasting models—ARIMA, SARIMA, and LSTM—were trained and evaluated to assess their predictive performance under realistic forecasting conditions.