A benchmarking study evaluating forecasting models under real market evolution. Demonstrates how near-perfect backtest accuracy can collapse under regime shift and highlights the importance of robust validation frameworks before deployment.

Key Insight: R² dropped from 0.99 (validation) to negative under real forward data.

Designed and deployed an imbalance-aware machine learning pipeline to detect fraudulent financial transactions with production-level precision. Achieved 84% fraud detection with minimal false alerts through ensemble modelling and executive dashboard integration.

Key Insight: Extreme class imbalance can hide fraud risk; imbalance-aware ensemble models detect fraudulent transactions while keeping false alerts near zero.

Sentiment analytics pipeline for customer reviews, uncovering product pain points and enabling automated monitoring of satisfaction trends.

Key Insight: Sizing and fabric issues emerge as the strongest drivers of negative customer feedback.

Machine learning system for early identification of bank customers at risk of churn, enabling targeted retention actions based on interpretable drivers of customer behavior.

Key Insight: Customer complaints are the dominant driver of churn, highlighting the importance of service recovery for retention.

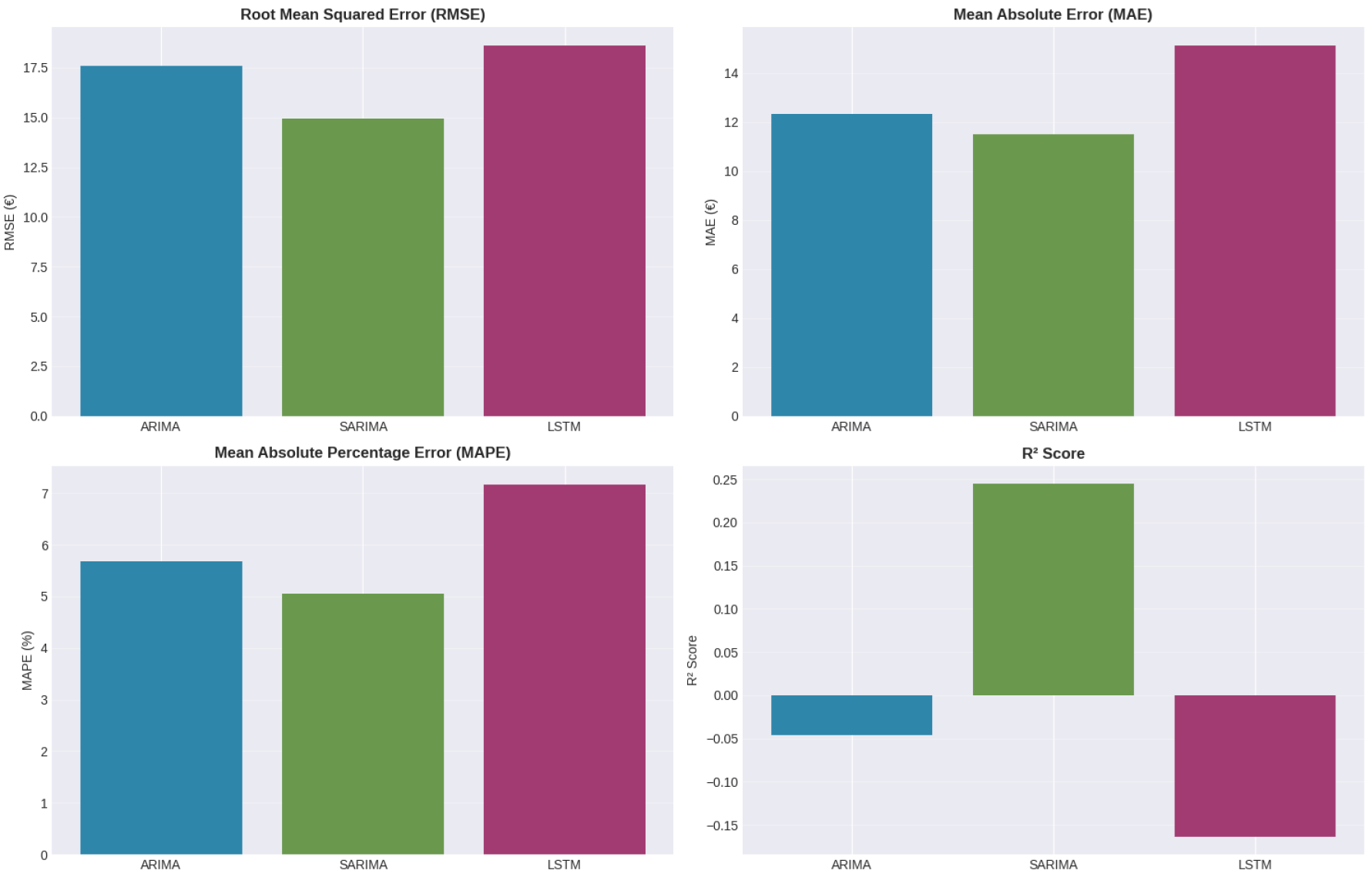

Comparative evaluation of statistical and deep learning models (ARIMA, SARIMA, LSTM) for medium-term stock price forecasting using historical market data.

Key Insight: Seasonal statistical models outperform deep learning approaches on limited financial time-series datasets.

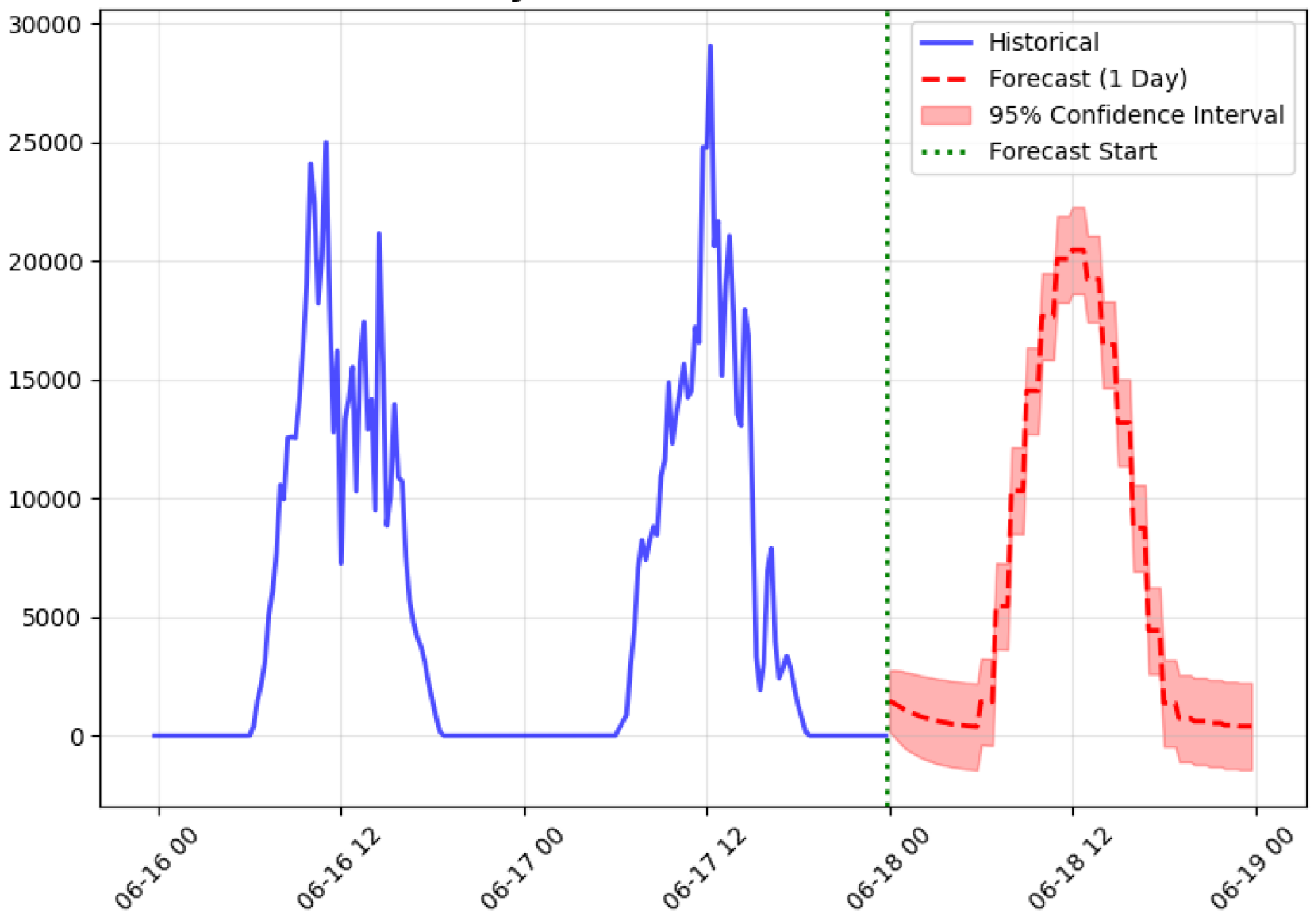

Forecasting solar power generation using weather data and time-series models to support grid planning and renewable energy management.

Key Insight: Weather-aware ARIMAX forecasting captured daily solar production cycles with high predictive accuracy.