Financial Analytics · Model Risk

Robust forecasting validation under structural market shifts.

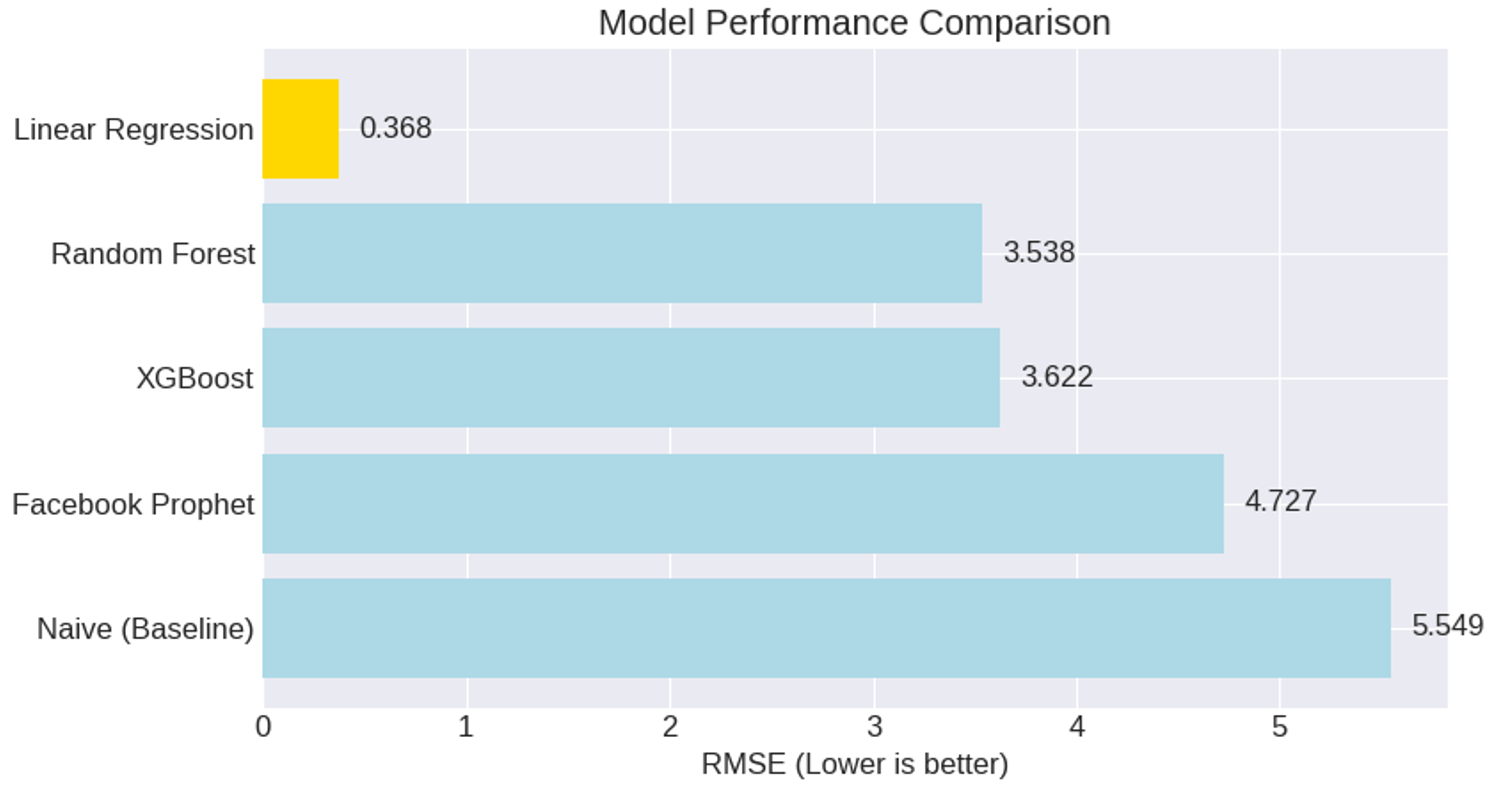

Many forecasting models demonstrate near-perfect performance in backtesting environments but fail under structural regime shifts. Businesses relying solely on validation metrics risk deploying unstable models that degrade rapidly under evolving market conditions.

We conducted a structured benchmarking study comparing classical statistical and machine learning forecasting approaches. Models were evaluated using both validation (backtesting) and forward testing frameworks to assess stability under regime shift conditions. Performance was measured using RMSE and R² to highlight discrepancies between historical accuracy and real-world robustness.